Politicians Gamble as Investors #5

Do Sovereign Wealth Funds do more harm than good?

Happy Tuesday (🧐). Welcome to the 5th edition of the Pomegranate Seed!

In the 4th edition of the Pomegranate Seed, I spent some time describing Lebanon’s economical meltdown.

The number one contributing factor to the meltdown was greed.

When politicians, or bankers who influence politicians, begin raising capital or deploying capital through non-traditional “financial engineering” schemes, it ends up doing more harm than good.

For developing countries, the main source of investment capital is through sovereign wealth funds (SWF). SWF’s include the ability to fund projects at home, create greater savings for future generations, help stabilize the domestic economy, and earn returns beyond those traditionally earned on foreign currency holdings.

Technically, there is nothing wrong with these types of funds. They provide tax benefits, wealth security, and insurance to millions of people around the world. But remember, who manages these funds.

With trillions of dollars being raised and deployed by politicians and bankers around the world, why are countries still failing to secure financial security for their citizens?

Income inequality, poverty, the lack of information & innovation: they still run rampant around the world today.

Politicians who use taxpayer money for investment capital continuously fail to achieve their goals and mandates. A majority of the world’s largest sovereign wealth funds and pension funds lack transparency and adequate governance. Proponents of these types of funds claim to bring the fortunes of capitalism to everyday citizens but often end up defrauding them.

But remember, we only do optimistic takes here.

There are many examples of Sovereign Wealth Funds that have lifted their countries’ citizens’ standard of living. If correctly implemented, SWF’s stabilize a country's economy through diversification and generate wealth for future generations. What can a landlocked county like Armenia achieve with a sovereign wealth fund?

Well, the possibilities are endless.

I kindly ask you to share this week’s article. Sovereign Wealth Funds highlight how politicians can easily gamble taxpayer dollars in underperforming investments. Without any accountability, these funds often end up hurting the average citizen over and over again. But if managed properly according to international standards, countries like Armenia can be propelled from the 20th century to the current one.

How did Sovereign Wealth Funds become so important?

To put it simply: Frightened sellers cause market crashes. An unexpected economic event, catastrophe, or crisis triggers the panic. This pushes sellers to sell quickly, trying to find buyers who can bail them out.

In 2008, following the mortgage crisis that crashed international markets and strapped around the world, who came to the rescue of the world’s biggest banks?

TA-DA! In come the “White Knights:” Sovereign Wealth Funds.

Kuwait’s sovereign wealth fund invested $3billion into Citigroup

GIC, an investment arm of Singapore’s government, invested $1billion into Citigroup

Abu Dhabi Investment Authority (ADIA), invested $7.5bn in Citigroup bonds.

International Petroleum Investment Company, which is wholly owned by the Abu Dhabi government, took a £2 billion investment into Barclays.

China Investment Corporation invested $3billion into the Blackstone Group

China Investment Corporation's invested $5billion in Morgan Stanley.

Singapore's GIC spent more than £5.5bn on a 9% stake in UBS.

Merrill Lynch received $5 billion from Singapore’s Temasek Holdings.

While there is no generally agreed-upon definition of an SWF, the U.S. Department of the Treasury defines SWF’s as government investment vehicles funded by foreign exchange assets that are managed separately from official reserves.

More colloquially, SWFs are investment funds controlled by governments.

One example is the Norwegian Government Pension Fund; much of its funding comes from oil revenues. Other SWFs such as the Government of Singapore Investment Corporation are funded through foreign exchange reserves.

The table below shows the largest SWF’s in the world in 2019. Notice that only Norway’s fund and Singapore’s’ Temasek Holdings are internationally certified and accounted for.

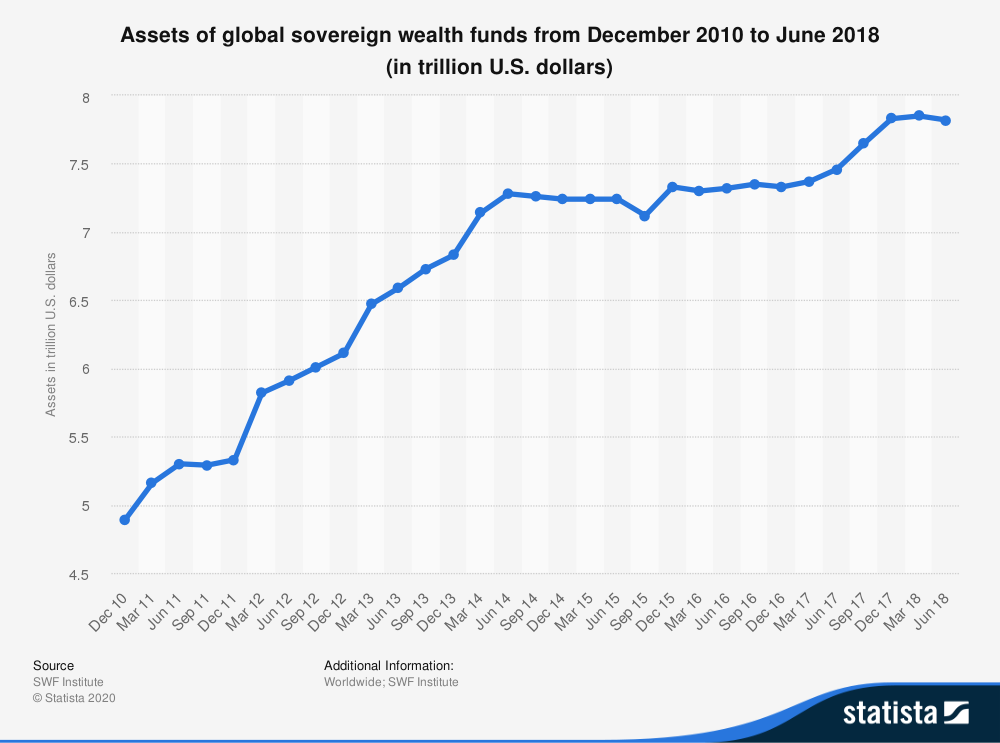

You read that right. Norway, China, and Abu Dhabi’s SWF’s combined have over $3 trillion dollars in assets.

Collectively, SWFs continue to hold significant weight and influence in global markets. State Street estimates that the top 35 SWFs in the world hold 6.8% of the global listed equity market. Furthermore, on a very conservative assumption that a quarter of SWF’s alternative portfolio is in private equity funds or deals, they appear to be holding 14% of the global private equity market.

Among the top asset owners in the world, they are unique in having no specific liabilities, which contributes to them having the highest allocation to alternatives of all key asset owner types.

In the United States and Europe, many political leaders assert that sovereign wealth funds pose a threat to national security, and their lack of transparency has fueled this controversy. The United States addressed this concern bypassing the Foreign Investment and National Security Act of 2007, which established greater scrutiny when a foreign government or government-owned entity attempts to purchase a U.S. asset. ( TIK TOK is the biggest example today.)

Why would a country start an SWF?

Savings funds that share wealth across generations by investing the proceeds from nonrenewable assets (often oil) into a variety of assets to fund long-term objectives and future generations;

Reserve investment corporations that are designed to increase the net returns to holding foreign exchange reserves;

Development funds that are designed to fund infrastructure and other socioeconomic projects;

Pension reserve funds that invest to fund the government’s pension-like liabilities.

Like other investors, SWFs hope to achieve these goals by using financial markets to diversify risk, to transfer funds through time, and to maximize returns.

The first sovereign wealth funds were created by oil-rich Gulf states to invest their structural surplus in European and North American financial markets. By taking their oil revenues and investing in foreign markets, the oil-exporting Gulf states were limiting inflationary pressures and currency appreciation. So far, export-focused Asian countries with sovereign wealth funds like China have been following the same policies.

Based on the current Sovereign Investors world map, Sovereign Investors in the Asia Pacific (especially China), the Middle East, and Africa are expected to account for a larger share of assets in 2020 than they do today. Sub-Saharan Africa is expected to show the largest growth in terms of percentage; however, it is starting with a much smaller asset base.

Concerns about SWFs

Because SWFs are controlled by governments, critics have been concerned that their investment strategies may be politically motivated and potentially conflict with the national interests of the countries in which they invest.

These concerns have increased with the size of the SWF sector and with the establishment of SWFs by strategically important countries, such as China and Russia.

Sponsoring countries argue that SWFs are motivated by a desire to maximize investment returns, not political ones. Because many SWFs do not publicly reveal their investments, the evaluation of these claims has proven difficult.

The famous oil baron John Paul Getty once defined his secret to success in three parts, "Rise early, work hard, strike oil."

The discovery of oil in developing nations was originally considered a resource blessing as scholars hypothesized that the revenue generated by oil exports would usher in an era of political and economic development throughout the emerging markets.

These predictions have not come to fruition; and today many of the emerging market countries remain economically-reliant on oil exports and dominated by authoritarian regimes.

What if Venezuela had saved some of the oil money?

Venezuela has toyed with the idea of an oil-stabilization fund, once.

In 1998, the year before Chávez came to power, the government set up the Fondo de Estabilizacion Macroeconomico (FEM). Money went in for a few years, but was soon drawn down again; the FEM has been dormant since 2003.

Now let’s assume that the government put 10% of its oil income from Petróleos de Venezuela, S.A. (PDVSA) into a reconstituted oil fund (call it the Hugo Chávez revolutionary fund 😒) starting in 2007.

Let’s assume too that Venezuela achieved a nominal return of 5% a year on its investments. By investing wisely and topping up the fund with extra cash every year, the pot would have built quickly, from $4.3 billion at the end of the first year of saving to $26 billion in 2012.

The fund would stand at almost $50 billion in 2020 and $92 billion in 2030.

An annual allocation of $3 billion would mean those numbers go up to $70 billion and $150 billion respectively.

Assume $5 billion a year and pretty soon you're talking serious money--enough to counter the economic cycle without losing control of the public finances.

Expecting Venezuela to behave like Norway, which has the world’s largest sovereign wealth fund, is clearly unrealistic. The collapse in global demand for fuel and U.S. sanctions will cause oil output to the crater, hampering the chief engine of economic activity and the key source of foreign exchange. Nicolás Maduro’s undemocratic regime has cut Venezuela off from the outside world for years, destroying the economy and depleting the health care system. Inflation is estimated to have been 6,567% in 2019, and according to the UNHCR, some 4,000 to 5,000 Venezuelans leave the country every day.

Beyond these factors, the greatest force for change in Venezuela will be the oil price. With a global surplus of supply and more OPEC cuts in the horizon, Venezuelan oil is no longer needed in the market. Without substantial export earnings, the government in Caracas is unlikely to be able to provide the investment needed to maintain current production, let alone meet Mr. Maduro’s target.

Even the most authoritarian regimes cannot survive without revenue.

How can a country like Armenia start a SWF if it has no oil money?

Singapore, just like Armenia, did not have pre-existing national wealth in the form of assets like oil to turn into money. So where does Singapore get its “national wealth”?

Singapore is a tiny, Southeast Asian city-state situated at the southern tip of the Peninsula Malaysia. It has no natural resources, just like Armenia.

Unlike Armenia, Singapore is affluent. It also helps that Singapore is surrounded by oceans.

It is the world’s fourth-leading global financial center

Operates the world’s best airport

One of the world’s top oil refineries,

Its Gross Domestic Product (GDP) per capita income is the third highest in the world, ahead of its former colonial master, the United Kingdom, as well as the United States.

In building the young nation, the Singapore leaders with Lee Kuan Yew at the helm began aggressive industrialization to develop the country’s manufacturing and export sectors. These measures were helped along by the rapid expansion of the world economy, which gave Singapore an economic boom through the 1960s and 1970s. It transitioned from a predominantly labor-intensive manufacturing economy in the 1960s and 1970s to skill- and knowledge-based economy in the 1990s.

The process of industrialization and the aggressive bid to develop the economy saw the Singapore government taking on stakes in various local companies, start-ups, and joint ventures, just like Armenia today.

Singapore began investing in its human capital, taking every dollar made abroad and domestically and reinvesting retained earnings strictly within the country. However, without achieving stability and peace, 25 years of highly specialized reinvesting in human capital in Singapore would not be possible.

Surrounded by neighbors many times its size that is strikingly different in terms of population makeup, religions, and languages, laden with unpleasant memories from the days of confrontation with Indonesia and its rancorous split with Malaysia, Singapore was determined to arm itself to secure its sovereignty. However, defense spending is extremely costly.

Singapore has managed to keep its defense spending at such high levels without compromising its fiscal soundness or resorting to punishing taxation. Indeed, quite the reverse: Singapore has constantly been ranked the best country for doing business globally.

That leaves the question: What is the balancing factor in the equation? The answer: sovereign wealth funds.

Under Article 142(1A)(b) of the Constitution of the Republic of Singapore, the government is able to use up to 50% of the net investment returns of SWF’s to supplement its spending in the annual budget.

50%

To put that in perspective, Singapore’s GIC fund alone returned 5.5% in 2019, equaling $5 billion in profit. From one fund alone, the Singapore government was able to use $2.5 billion to fund social programs. The entire defense budget for the Republic of Armenia is roughly $600 million dollars.

Many lessons about the operation of SWF’s are to be drawn from the Singapore experience, especially the need to clearly orient SWF’s toward serving national interests, the advantages of taking a long-term approach to invest, and the benefits of adopting transparency in portfolio risk management.

Ultimately, however, SWFs can be no more than tools of national strategy. The strategy itself and the national interests they serve remain the preserve and the responsibility of political leadership. Only a confident, responsible, and competent political leadership can adequately define national interests and have the discipline to steward national resources in their service.

By following Singapore’s economic roadmap, Armenia can achieve international financial stability, invest in human capital, finance its military without the help of Russia, and maintain its business-friendly tax climate to attract investment.

In the next edition of the Pomegranate Seed, I’ll propose an investment guideline as well as a “roadmap” for policymakers considering setting up an SWF for Armenia.

Blog/News Roll

I’ll be sharing a list of websites/people sharing extremely important information regarding Armenia. Expect this list to grow with every single publication.

DataArmenia

Armenian Military

Economist Intelligence Unit

EvnReport

Emil Sanamyan

Dr. Artyom Tonoyan

Dr. Aleksandr V. Gevorkyan

MFA of Artsakh

Artsakh / Karabakh Human Rights Ombudsman

__

Jad Chaaban

Federal Reserve Economic Data

Sovereign Wealth Fund Institute

Investopedia

CONSTITUTION OF THE REPUBLIC OF SINGAPORE

CONSTITUTION OF THE REPUBLIC OF ARMENIA

__